Beyond Age and Income: How Needs-Based Segmentation Uncovers True Consumer Motivation

August 25th, 2025

Introduction

In the rapidly evolving world of marketing, understanding consumer behavior is pivotal to success. As businesses strive to cater to diverse consumer needs, segmentation becomes essential. Let’s explore the concept of needs-based segmentation—what it is, why it’s valuable, and how it can be applied to the banking industry, using insights from a national consumer survey that TRC conducted with Rice University.

What Is Needs-Based Segmentation?

Needs-based segmentation is a way of grouping customers based on the specific problems they want to solve or the benefits they’re looking for—rather than on basic facts like age, gender, or income. It focuses on understanding what truly drives their decisions, such as convenience, trust, value, or support. Unlike more common methods, it allows for cross-demographic groupings, meaning customers with very different backgrounds may share the same needs.

What Are the Benefits of Needs-Based Segmentation?

Needs-based segmentation helps businesses understand why customers make decisions by grouping them based on their underlying motivations and priorities, rather than just demographics. Needs-based segmentation is a powerful tool that leads more relevant and engaging marketing communications and product and service designs that better meet customer needs. Because it centers on motivations, it can uncover new opportunities, highlight underserved segments, and offer a competitive edge by helping brands connect with customers in a more meaningful and authentic way.

Example of Needs-Based Segmentation

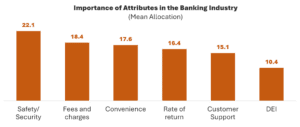

To illustrate the power of needs-based segmentation, consider the following example from the banking industry. As part of a larger research project on value drivers done in conjunction with Rice University, a national sample of 500 consumers provided input on banking services. Each respondent was asked to allocate 100 points across 6 attributes based on importance when choosing or continuing to use a bank for deposit accounts.

When examining the allocations across all respondents, Safety/Security is ranked as most important of the 6 attributes.

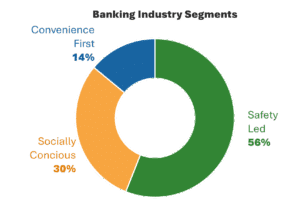

However, needs-based segmentation finds that this doesn’t tell the whole story. The analysis revealed 3 distinct segments.

Safety Led (Segment 1): This is the largest segment, with safety and security ranked as the highest priority, highlighting the central role safety plays in the banking industry. Customers in this group likely view safety as a core function of a bank. While most attributes are relatively clustered together, safety is more important, and Diversity, equity, and inclusion (DEI) is notably less important than all other attributes.

Socially Conscious (Segment 2): This segment places greater emphasis on DEI than any other group. While only a small proportion rank DEI as their top priority, a majority consider it equally important to other key attributes suggesting that while it is not THE factor, it is important as part of a comprehensive set of core benefits. It’s worth noting that the study was conducted from March 3–12, 2025, during a time when DEI was a prominent topic in the United States; future studies may yield different results.

Convenience First (Segment 3): This group prioritizes convenience above all, and places above average importance on customer support. Their strong focus on convenience drives up the overall average for this attribute across all segments.

A correspondence map visually highlights the relationship between the three needs-based segments and the six attributes they value. Each segment is positioned near the attributes that are most strongly associated with it, allowing us to quickly see how preferences differ across the groups. The spatial distance between points reflects the strength of association. Segment 3 is positioned near convenience, suggesting they prioritize ease of access and simplicity in their banking experience.

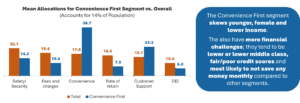

Let’s take a closer look into the Convenience First segment. Mean allocations compared to the overall population along with their unique demographic and financial profile are shown below.

Although this segment may face more financial challenges, it represents a large opportunity for banks due to its overrepresentation of younger consumers (39% aged 18–34, compared to 30% of the general population in the survey). Engaging Millennials and Gen Z early, while financial habits are still forming, is likely to lead to long term loyalty and value.

Offering convenience focused solutions such as seamless mobile access, early pay, or free ATM access can help banks meet immediate needs, support credit building and position themselves as trusted financial partners.

While the Convenience First segment reports relatively strong satisfaction (75%), it trails the other segments (79% and 81%), suggesting that convenience may not fully meet expectations. Given the segment’s high concentration of younger, likely underbanked, consumers especially women, banks have an opportunity to move beyond surface-level convenience and deliver experiences that build trust and keep customers around for the long haul.

Conclusion

Needs-based segmentation helps businesses understand what really drives their customers’ decisions. Instead of just looking at age or income, it focuses on the reasons behind consumer behavior. This approach can uncover important differences that other methods may miss. This specific needs-based segmentation highlights how meeting immediate convenience needs can unlock deeper, lasting relationships.

By using these insights, companies can create more meaningful marketing strategies that truly connect with their audience.

References: https://business.rice.edu/center-customer-based-execution-strategy. What Really Matters to Americans – the 2025 customer value report (a nationwide survey of 3,000 U.S. residents quantifies what they value across 18 business sectors), March 2025. In collaboration with TRC Insights.