That New and Annoying 3% Credit Card Surcharge: Finding Answers with Pricing Research

September 15th, 2025

Over the past few years, retailers have started adding a 2–4% “surcharge” to common purchases when the buyer uses a credit card to pay. I started noticing this 2–3 years ago at small shops, coffee spots, and local restaurants. Today, it’s become the norm in places like the Hamptons, a vacation destination outside of New York City, where nearly every coffee shop, restaurant, and retail store now tacks on 3–4% at checkout. Call me cheap, but I’m not a fan of paying more just because I use a credit card.

So, I’ve started carrying more cash, just to dodge that extra fee. I know I’m not alone. But I sure wonder how consumers in general are perceiving this extra charge. Here are some recent numbers regarding surcharges and consumer perception.

By the Numbers: Surcharges and Consumer Behavior

- Credit card surcharges are now legal in all but three U.S. states – Massachusetts, Maine, and Connecticut. The regulations and laws are constantly changing (Data from Merchant Cost Consulting Group).

- The surcharge rate can never exceed 4% of the total credit card transaction.

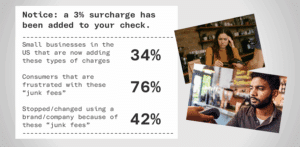

- 34% of small businesses in the U.S. are now adding surcharges to credit card transactions, according to a 2024 survey by J.D. Power among 3,841 U.S. small businesses. This is up from just 1-2% in 2019!

- Consumers report rising frustration with “junk fees” – 76% of U.S. consumers said junk fees have influenced their decisions about which companies to do business with, and 42% said they have changed or stopped using a specific company or brand due to junk fees. Survey was conducted with 2,000 respondents by Wise and Morning Consult.

Wait – Am I Paying the Surcharge Now?

As a marketing research expert and former small business owner, I know how it works. Processors like Stripe, Visa, and Amex charge businesses 2–3% to process credit card payments. But here’s the kicker—those fees have come down in recent years with competition from ShopPay and others. Some high-volume retailers pay as little as 1.5%. So, if you’re tacking on a 3% fee to my bill, you’re not just covering cost—you’re making a profit off my payment method.

I always assumed the “convenience charge” was for convenience. But who’s it more convenient for – me, the customer, or you – the business owner? I don’t want deal with dirty $1s and $5s, but I’m thinking that you don’t want to haul a bunch of small bills and coins to the bank each day either. Don’t pretend this fee is for my benefit. And as a side note…don’t get me started on pennies and nickels – why do they still exist? Maybe that is a topic for my next article 🙂

Cash Discount or Surcharge? Framing Matters

My initial reaction to all this – I feel ripped off. Do other consumers agree with me? Just charge me the 3% extra and don’t talk about it. Inflation is raging anyway, so if I go to a coffee shop, I won’t really notice if I pay $4.50 for my cold brew or $4.63. Although, brand managers and small business owners still need to be very careful about pricing thresholds. For example, a regular cup of drip coffee should NOT cost over $3.00. For a while that threshold was $2.00, but inflation busted that one up. Price elasticity also varies by category and purchase size too. Consumers will notice small increases on items they purchase frequently. That’s where pricing elasticity really kicks in—consumers react more strongly to increases on familiar, frequently bought items.

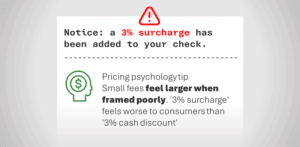

Here’s something marketers and behavioral economists have known for years: how you frame a price matters. Let’s stick with the coffee shop example. I go in and buy my favorite cold brew and donut. The price shown is $8.00, but I have cash, so I only end up paying $7.76. Now I think – cool, good deal. That could be framed as a “cash discount.” But, when the same purchase is listed as $7.50 and then I get hit with a 3.5% surcharge at checkout, I still pay $7.76, but it feels sneaky. Same math, different feeling. So, as we marketers know, framing the price is often times more important than the actual price.

Let’s Do Some Research with Consumers

So….what does all this mean? I sure have a lot of thoughts and opinions about the surcharge culture and hidden or junk fees. But, how do the rest of U.S. consumers feel?

Here at TRC Insights, we stay on top of consumer trends—especially those tied to digital payments. So, we’re running a national survey (N=1,000 gen-pop consumers) to explore awareness, attitudes, and behaviors around credit card surcharges.

Key Research Objectives:

- What are overall attitudes and awareness toward the 3% credit card surcharge?

- Do these fees impact consumer behavior?

- Which subgroups show more price elasticity? What groups are most sensitive to the fees?

More Coming Soon!

Credit card processing fees are now in plain sight. Businesses are increasingly shifting them to the consumer under the banner of “convenience.” But to many, it just feels like another hidden inflation tactic.

This trend is especially relevant in the context of broader inflationary pressures, where consumers are already sensitive to price increases. For FinTech and payment companies, understanding how these surcharges affect consumer behavior is very important. It has implications for digital payment adoption, consumer trust, transaction volume, and more.

Over the next few months, I’ll publish more insights from our pricing research. Got a hypothesis, a question, or just want to geek out over pricing strategy? Email me: tbenzing@trcinsights.com.

Here is part two of the Credit Card Surcharge articles series.

Sources:

Third of U.S. small businesses add credit card surcharges | Payments Dive