Credit Card Surcharges Are Here to Stay

December 18th, 2025

Presenting Real Data from 2025 Research Study

Hi everyone – I am back at it again with Part 2 of my blog posts on the topic of Credit Card Surcharges in the US. In the first article, we introduced the concept of businesses charging a fee of 2-5% when a credit card is used instead of cash. We learned that this practice is becoming more and more commonplace, although there is still a lot of grey area in regulations and legality; especially with regard to communication of these fees.

Now, we have some real data regarding credit card surcharges and consumer perceptions. In November 2025, TRC Insights ran an online survey with 961 consumers in the US. TRC is using this data to report on consumer attitudes and habits in the FinTech and digital payment space. The data is also being used to create digital twins that TRC and clients can utilize for future research.

What We Found – Primary Research from 2025 Study

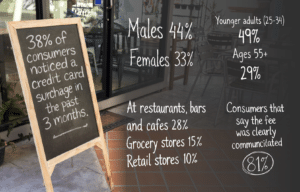

- 38% of consumers noticed a credit card surcharge on a purchase in the past 3 months.

- Males were more likely to notice the fee: 44% vs. 33% of females.

- Younger adults (25–34) were most aware: 49% noticed the fees vs. just 29% among those 55+.

- Where they noticed it most recently:

- 28% at restaurants, bars, or cafés

- 15% at grocery stores

- 10% at other brick-and-mortar retail stores

- 81% of consumers say the fee was clearly communicated; 19% say it was not.

- Among those who noticed:

- 47% still paid with a credit card

- 38% switched to debit or cash

- Only 1% abandoned the purchase entirely (very good news for business owners)

Overall, the results aren’t too surprising. Consumers are noticing fees, but not abandoning purchases because of them. And the fees are most commonly noticed at restaurants/bars/cafes, which makes sense to me, since this is where I have personally noticed the fees too.

Businesses are doing a good job with communication, and a lot of people still use a credit card to pay, implying that they are generally OK with the higher price. Or at least they aren’t changing habits too much because of the fees. Some do switch to debit card to avoid the fee, but that is a very minor change and doesn’t impact the transaction at all for the consumer.

Owners and marketing managers may want to also consider their audience, as there are some differences between gender and age groups.

Current Law and Practice – Example with New York State

The laws and regulations currently vary from state to state and are constantly changing. For example, in the State of New York (New York General Business Law § 518) merchants may charge a surcharge for credit card payments — but they must clearly and conspicuously post the “credit‑card price” (the total price including the surcharge) before checkout, or else show both a cash price and a credit‑card price side by side. Also, the surcharge may not exceed the actual processing cost the merchant incurs; anything beyond that is prohibited.

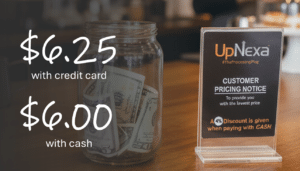

In a recent trip to East Hampton, NY, I saw the sign (shown below) at a coffee shop. I won’t name any names, but it is a nice coffee place that I like a lot. They position the fee as a way to “provide you with the lowest price” – Wow – what a great deal! I save 4% off my $6.25 coffee when I pay with cold hard cash. I’m kidding of course. I’m sure this business knows that at least two-thirds of the people walking in the door have no cash on them at all, therefore they have no choice but to pay the 4% extra.

As far as legality in NY State, this merchant does show the higher price and then discount based on a cash purchase. But, I sure would argue that 4% is considerably higher than the fee likely paid by the shop to the card processor, which would break the rules of NY state. Most of the big processors like Stripe, PayPal, ShopPay or Square charge somewhere in the 1.5-3% range depending on volume.

Connection to Pricing Research

With some pricing research, owners and marketing managers can minimize the negative impact of additional credit card fees.

TRC Insights has expertise conducting very complex pricing elasticity research; often times using conjoint analysis, where we can isolate and test different variables that have an impact on overall purchase intent. For retailers considering adding a surcharge to common purchases, we can help researchers design a study that will look at the impact of the surcharge relative to other variables.

Some research questions to think about:

- How can the marketer or small business owner think about these fees?

- What is the best way to communicate the fees to customers?

- How can they avoid negative sentiment and an unfavorable impact on brand equity?

There could be dozens of reasonable ways to communicate these fees to customers. At TRC Insights, we would recommend a pricing research study that incorporates consumer choice into simulated purchase exercises. We look at different variables and isolate them to see what is moving the needle with regard to purchase interest.

Here are some options that could be tested (ignoring legal issues for now, since they are on a state-by-state basis):

- Say nothing, just add in a fee when a credit card is used

- Communicate it as a “x% Credit Card Surcharge” or “Credit Card Fee” or “Convenience Charge”

- Communicate it as an “ x% Cash Discount”

- Just do away with the fee and charge everyone the 2-4% extra (I secretly think this is the best option, as consumers probably won’t even notice the small increase)

The results from this research could give insight into the best way to communicate credit card fees.

Conclusion

The reality is that credit card surcharges aren’t going anywhere soon. It is like highway tolls or temporary taxes…the businesses or government entity collecting the money becomes used to the extra revenue and depends on it over time.

We’ll keep publishing more data and insights on this topic—and if you have a question or want to dig deeper into the data or pricing strategy, feel free to email me at tbenzing@trcinsights.com.

Sources:

Primary data survey conducted by TRC Insights in November 2025

New York State Senate Website – www.nysenate.gov/legislation/laws/GBS/518